Blog Details

Switching to solar power is no longer a futuristic idea—it’s a present-day reality with long-term payoffs. But for many homeowners, the big question isn’t whether to go solar. It’s about how to afford it. Solar financing has evolved to give you multiple options that can work with different income levels, credit scores, and savings goals. Whether you’re looking to buy, borrow, or rent your way into clean energy, understanding the differences between a solar loan, solar lease, and Power Purchase Agreement (PPA) will help you make the most out of your investment—and your energy bills.

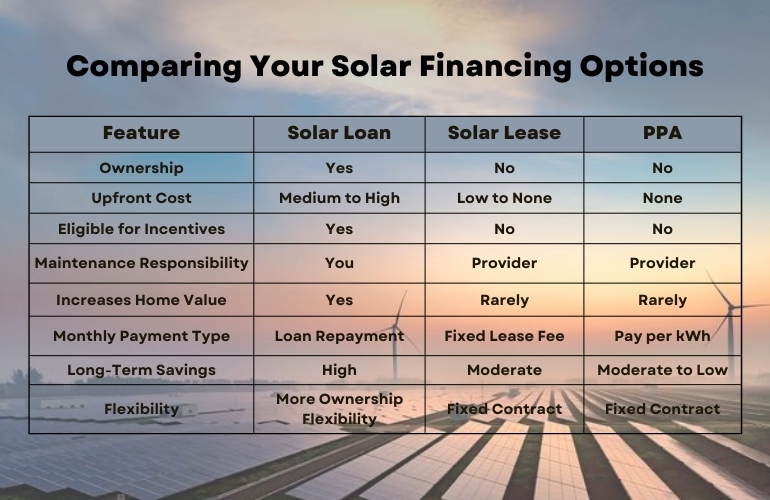

Solar Loans

If you’re aiming to own your system fully, solar loans give you that path while spreading out the cost. Think of it like a mortgage or car loan—you make monthly payments over time until it’s yours.

What’s in it for you?

You get access to solar tax credits, solar rebates, and other government solar incentives that come with ownership. This lowers your net cost and shortens your solar panel payback period. Once the loan is paid off, your electricity costs virtually disappear—your panels are still working, and your wallet isn’t.

Long-term benefits include:

- 1. Increased home value

- 2. More control over your solar panel system

Access to net metering, so you can earn credits for the excess power you send back to the grid

What to consider:

There’s typically a down payment, and you’ll be responsible for maintenance. Plus, your solar loan interest rates and credit score will play a role in your eligibility. But if you qualify, the long-term solar savings often outweigh these early commitments.

Tip: Use a solar panel cost savings calculator to estimate how much money you’ll save over time compared to your monthly loan payments.

Solar Leases

With a solar lease, you don’t buy the system—you rent it. You pay a monthly fee to use the solar equipment on your roof, while the leasing company owns and maintains it.

Why go this route?

There’s little or no upfront cost, and you won’t have to worry about repair bills or system upkeep. This option is designed to give you predictable monthly payments and easy access to solar without major commitments.

But here’s the catch—you’re not eligible for solar tax credit eligibility, and your savings are limited to what you get from using solar instead of utility power.

You’ll want to ask yourself:

- 1.How long do I plan to live in this house?

- 2.Am I okay with not owning the panels?

- 3.Will these changes affect my home’s resale value?

Keep in mind: leased solar systems may not significantly increase your home value because the next buyer has to agree to take over the lease.

Power Purchase Agreements (PPAs)

In a PPA, a solar company installs and maintains the panels on your property, and you pay only for the electricity the system generates, usually at a lower rate than your local utility.

The upside?

- 1. Zero upfront costs

- 2. Lower kWh rate than your utility

- 3.Maintenance is included, just like a lease

If your primary goal is to reduce your power bill without owning the system, this model is ideal. However, PPAs come with their limits. Like leases, you won’t qualify for solar panel grants and subsidies, and you won’t build equity in the system. Furthermore, look out for rate escalators in your contract—these allow the solar provider to increase your energy price annually, sometimes canceling your original savings.

Comparing Your Solar Financing Options

Government solar incentives

What’s Best for You?

Your greatest bet if you want complete control and the most long-term advantage is a solar loan. Use tools to calculate your solar ROI and see how quickly your investment pays off. Leasing can be your fit if you want low-risk access to solar electricity without the upfront cost. It works well if you don’t qualify for loans or you’re not ready to deal with system upkeep.

If you want the lowest barrier to entry and don’t mind just paying for power, a PPA provides a low-commitment route to clean energy—but be sure to review your rate terms carefully.

Remember also that there are fine solar financing firms specialized in customized programs, and low-income households have solar financing choices. Search for flexible-term solar panel financing schemes, particularly if your budget is limited.

Conclusion

Going solar is about making wise financial decisions rather than only about doing the right thing for the world. Whether your inclination is for a PPA, a lease, or a solar loan, there is a route that will work for your house, income, and way of life. From uncertainty to clarity—and start running your house on your terms—you may move using resources like a calculator for solar panel cost savings, clear information about solar loan alternatives, and access to government solar subsidies.